IRD misleads taxpayers with or without agents

[this article published 5 March 2024, with some subsequent minor edits based on feedback]

IRD’s job is to collect tax, and in fact the maximum to boot.

But that responsibility comes with critical conditions.

In administering the tax system IRD routinely abuses those responsibilities.

The issues set out in this article, we and no doubt many other tax advisors have raised with IRD on many, many occasions. IRD’s reaction ranges from immediate agreement, to ‘will give consideration’, to outright rejection. Whatever staff say, there is no action.

Our professional bodies – CAANZ, CPA and ATAINZ do not appear to be willing to challenge IRD.

Examples:

- Self assessment regime

- NZ operates a ‘self assessment ‘ regime whereby taxpayers prepare their own tax returns, and IRD then has generally four to five years to reopen and propose any amendments.

- The principles were formally introduced in a 1998 Government discussion document, which stated (inter alia)

- The central proposal in this discussion document is to enact legislation requiring taxpayers to assess their own income tax liability in accordance with the core provisions in Part B of the ITA.

- However that is not the way it works in practice. IRD systems often issue tax assessments and then rush to payment demands or refunds relying on the taxpayer to know whether there are other assessable income or expense items that haven’t been included. That requires an unrealistic level of tax expertise.

- IRD invites the taxpayer to amend their tax assessment and provides a basic level of guidance (IR1066) which doesn’t cover many of the common items that arise.

- Without further guidance how can a taxpayer know whether an item is capital/revenue, exempt, affected by a double tax agreement etc.

- We are often called on to assist in untangling a mess where taxpayers were unaware they derived assessable income (e.g. some foreign pensions, overseas rental or trading), or equally problematic, exempt income (e.g. some other foreign pensions) which was added to the tax return by the taxpayer.

- Principles were raised around 30 years ago by the then NZ Society of Accountants which recommended that IRD issue a pro forma tax return, but with the critical override that the taxpayer have the opportunity and indeed obligation to disclose any other assessable income or deductible expenses, and then (and only then) attest that the return was full and correct.

- IRD ignores the override and pretends that IRD’s default assessment is true. in fact IRD has the audacity to describe the auto return as being ‘submitted’ or ‘lodged’. See further under role of tax agents.

- IRD states

- Some signs that someone else might be using your IRD number are:

- …

- You have received a notice of assessment from us for a return you did not file.

- A return you have not filed is showing as filed

- see www.ird.govt.nz/managing-my-tax/scams/signs-of-a-scam

- Some signs that someone else might be using your IRD number are:

- Ironic given that IRD itself does exactly that

- In reports provided to tax agents, IRD documents the date of their made up auto assessment (again pretending a return has been filed), and not the date of a correct return subsequently filed by the taxpayer.

- Technical advice

- IRD’s job is to collect tax. It is most definitely not to provide advice. We have caught IRD telling taxpayers how legislation works and most definitely getting it wrong.

- If there is ever a situation where IRD identifies that a taxpayer needs technical advice, IRD should say so. However in general IRD doesn’t do that but instead points them to the IRD website. Taxpayers usually don’t have the expertise to apply tax laws to their own circumstances in the many complex areas of taxation – think here of tax residency, property transactions, foreign investments among many, many others – leaving them to flounder and exposing them to errors.

- From time to time taxpayers submit section 113 adjustment requests where we have identified they have unknowingly overstated their tax obligation. IRD is far less willing to accept those applications than they are to accept voluntary disclosures of underpaid tax, and the latter often involve wasteful interaction.

- IRD takes the position that taxpayers should know how tax rules apply to their circumstances. If they haven’t identified an option that correctly results in a lower liability that is their fault and it’s not IRD’s problem. We still see reference to ‘regretted choice’ notwithstanding IRD’s own publications.

- In our view IRD should actively encourage appropriate taxpayers to seek expert advice.

- Provisional tax

- In very broad terms, taxpayers with more than around $20,000 of taxable income, which hasn’t been taxed at source, must generally pay tax as they go through the provisional tax system.

- In general provisional tax is based on the most recently filed tax return plus an uplift.

- For example in the year ending 31 March 2025 a provisional taxpayer will base provisional tax on the residual income tax charge[1]for the year ended March 2024 plus 5%.

- If the 2024 return hasn’t been filed (and keep in mind that could be 12 months after balance date), then they use the year ended March 2023 plus 10%. However, in that situation IRD systems incorrectly show nothing due. Any tax credits are shown as ‘held’ with no clue as to why.

- If a taxpayer instead believes IRD systems and doesn’t pay the instalments, IRD will later charge backdated interest and penalties, despite their own notifications being wrong!

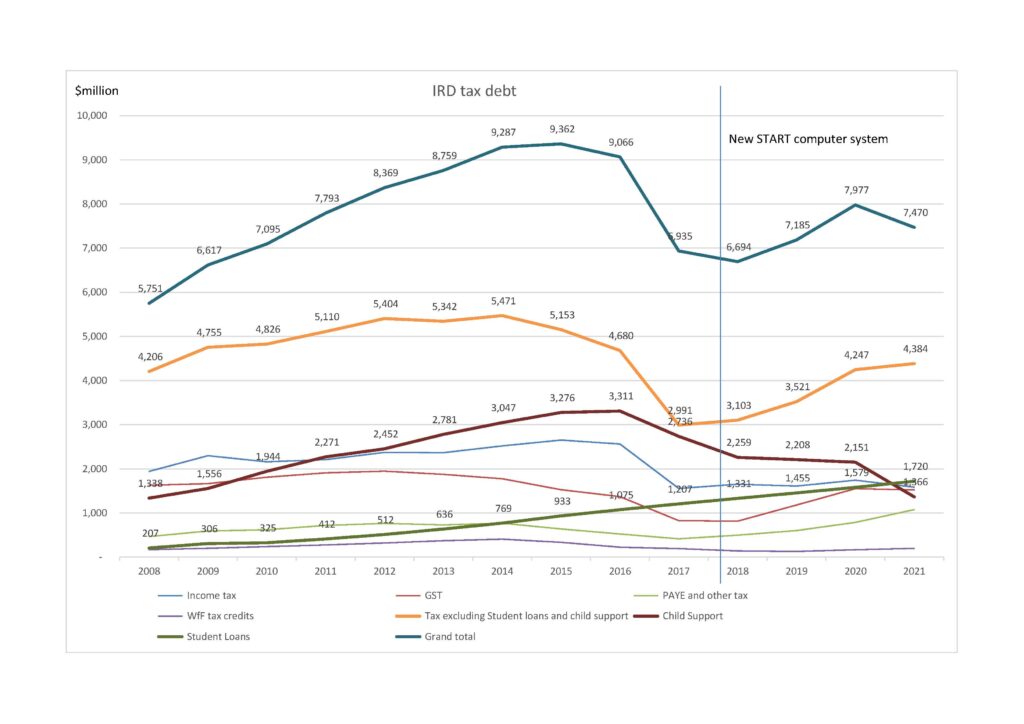

- Tax owing

- When a taxpayer owes tax, IRD shows it as owing without distinguishing between tax due now, overdue or a long way in the future,

- IRD also sprinkles those debt indicators with exclamation marks and orange emergency triangles (normally used to signify serious physical danger) as if they are all urgent. Almost inevitably any high priority items are lost in a fog of detail.

- Often IRD doesn’t allocate debt demands between income years.

- Where back tax is owed it is often legally possible to purchase back tax credits from a central pool administered by the Public Trust. IRD is able to tag the file to identify such an application has been made but in general does not activate that, and continues with payment demands.

- We have even caught IRD contacting an employer direct and requiring tax to be deducted from salary where there was a payment arrangement in place.

- Premature refunds

- If a taxpayer pays into an incorrect period, IRD systems are very quick to grab the payment, offset against an obligation that is not yet due, and then refund the rest. The hoops involved in getting the payment directed to the right account are time consuming.

- Surely the $1.7bn system could check the accounts in real time, identify the apparently incorrect destination and alert the payer before it is processed.

- Gross overuse of electronic correspondence

- IRD supplants genuine communications with gross overuse of electronic letters and messages so that genuine information is lost in a fog of rubbish.

- Dear Commissioner – after you got no reply to the tenth letter did you consider whether a different approach might be warranted?

- Email communications

- IRD published policy when sending an email is to automatically request a read receipt, and conversely to provide a read receipt when asked.

- IRD staff often do not extend the latter courtesy.

- Misleading priority

- As noted above, IRD electronic communications are sprinkled with exclamation marks in orange triangles – whether they are notifying ten million dollars overdue or a GST return due in two months.

- Telephone communications

- IRD technical staff almost never answer the telephone. Instead their phone just goes to an anonymous voicemail, with no clue as to whether staff are at work, on leave, or (sometimes) have left the role altogether.

- In general IRD systems block caller ID and staff only give their first name, expecting us to provide confidential information. “Hi its Bob here from IRD, please tell us everything about your client”

- Use of junior staff

- IRD uses junior or inexperienced staff to front communications,

- the real decision makers are hiding in the shadows.

Role of tax agents

The above issues are exacerbated by IRD thumbing its nose at the critical role played by tax advisors and agents.

- Taxpayers whose income is solely from NZ with tax deducted at source do not need an agent (until something changes and catches them unawares for tax).

- Most other taxpayers do need assistance, and for that reason will often engage a tax advisor and/or agent.

- When a taxpayer has a tax agent, IRD routinely bypasses that relationship by contacting the taxpayer directly by electronic letters and messages. Bad enough if the information is correct, but borders on criminal when the information is wrong, as is often the case.

- At a tax conference a few years ago the then Commissioner had the audacity to claim that a significant proportion of tax agents preferred IRD to contact their clients directly in respect of tax debt. This was a blatant lie and on challenge was quickly withdrawn. It does however illustrate an underlying theme of IRD’s disregard for the critical role provided by tax agents.

We strongly recommend a thorough independent review of the way that IRD interacts with taxpayers and their authorised representatives.

[1] Annual tax charge less tax withheld at source